Page 43 - Nuvama | IC Report 2023

P. 43

INDIA: THE 5D ADVANTAGE

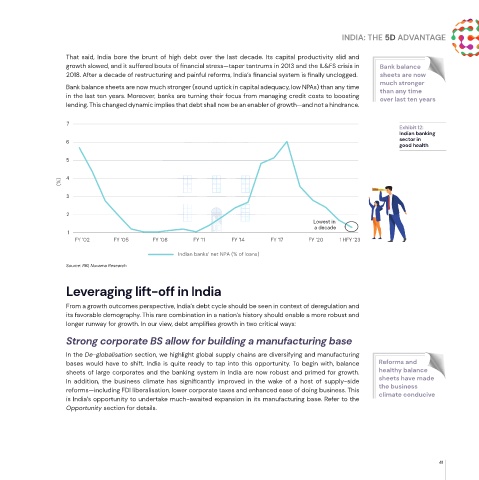

That said, India bore the brunt of high debt over the last decade. Its capital productivity slid and

growth slowed, and it suffered bouts of financial stress—taper tantrums in 2013 and the IL&FS crisis in Bank balance

2018. After a decade of restructuring and painful reforms, India’s financial system is finally unclogged. sheets are now

much stronger

Bank balance sheets are now much stronger (sound uptick in capital adequacy, low NPAs) than any time than any time

in the last ten years. Moreover, banks are turning their focus from managing credit costs to boosting over last ten years

lending. This changed dynamic implies that debt shall now be an enabler of growth—and not a hindrance.

7

Exhibit 12:

Indian banking

sector in

6

good health

5

(%) 4

3

2

Lowest in

a decade

1

FY ‘02 FY ‘05 FY ‘08 FY ‘11 FY ‘14 FY ‘17 FY ‘20 1 HFY ‘23

Indian banks’ net NPA (% of loans)

Source: RBI, Nuvama Research

Leveraging lift-off in India

From a growth outcomes perspective, India’s debt cycle should be seen in context of deregulation and

its favorable demography. This rare combination in a nation’s history should enable a more robust and

longer runway for growth. In our view, debt amplifies growth in two critical ways:

Strong corporate BS allow for building a manufacturing base

In the De-globalisation section, we highlight global supply chains are diversifying and manufacturing

bases would have to shift. India is quite ready to tap into this opportunity. To begin with, balance Reforms and

sheets of large corporates and the banking system in India are now robust and primed for growth. healthy balance

In addition, the business climate has significantly improved in the wake of a host of supply-side sheets have made

reforms—including FDI liberalisation, lower corporate taxes and enhanced ease of doing business. This the business

climate conducive

is India’s opportunity to undertake much-awaited expansion in its manufacturing base. Refer to the

Opportunity section for details.

41