Page 42 - Nuvama | IC Report 2023

P. 42

• DE-GLOBALISATION • DEREGULATION • DEBT • DEMOGRAPHY • DEMOCRACY

Of these policy choices, we think allowing higher inflation and suppressing the cost of capital (negative

real rates) may eventually be the path of least resistance. If so, and financial repression emerges as a

policy of choice over time, then countries with strong balance sheets, not-so-high indebtedness and

expanding workforce shall be the ones that attract capital. India is a no brainer; it ticks off all the boxes.

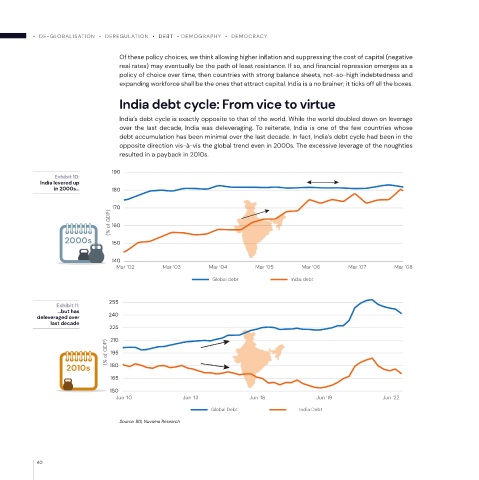

India debt cycle: From vice to virtue

India’s debt cycle is exactly opposite to that of the world. While the world doubled down on leverage

over the last decade, India was deleveraging. To reiterate, India is one of the few countries whose

debt accumulation has been minimal over the last decade. In fact, India’s debt cycle had been in the

opposite direction vis-à-vis the global trend even in 2000s. The excessive leverage of the noughties

resulted in a payback in 2010s.

190

Exhibit 10:

India levered up

in 2000s… 180

170

(% of GDP) 160

2000s 150

140

Mar ‘02 Mar ‘03 Mar ‘04 Mar ‘05 Mar ‘06 Mar ‘07 Mar ‘08

Global debt India debt

255

Exhibit 11:

…but has

deleveraged over 240

last decade

225

(% of GDP) 210

195

2010s 180

165

150

Jun ‘10 Jun ‘13 Jun ‘16 Jun ‘19 Jun ‘22

Global Debt India Debt

Source: BIS, Nuvama Research

40