Page 117 - Nuvama | IC Report 2023

P. 117

INDIA: THE 5D ADVANTAGE

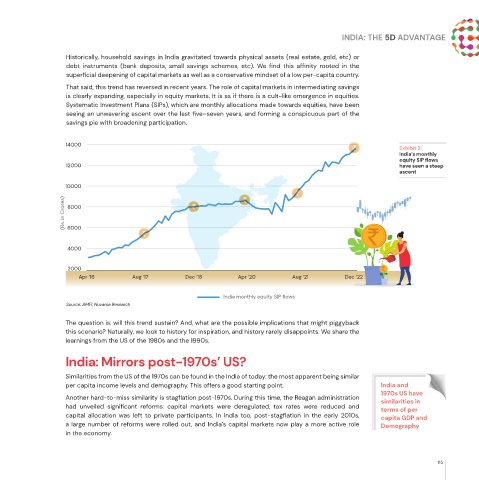

Historically, household savings in India gravitated towards physical assets (real estate, gold, etc) or

debt instruments (bank deposits, small savings schemes, etc). We find this affinity rooted in the

superficial deepening of capital markets as well as a conservative mindset of a low per-capita country.

That said, this trend has reversed in recent years. The role of capital markets in intermediating savings

is clearly expanding, especially in equity markets. It is as if there is a cult-like emergence in equities.

Systematic Investment Plans (SIPs), which are monthly allocations made towards equities, have been

seeing an unwavering ascent over the last five–seven years, and forming a conspicuous part of the

savings pie with broadening participation.

14000

Exhibit 2:

India’s monthly

equity SIP flows

12000 have seen a steep

ascent

10000

(Rs. in Crores) 8000

6000

4000

2000

Apr ‘16 Aug ‘17 Dec ‘18 Apr ‘20 Aug ‘21 Dec ‘22

India monthly equity SIP flows

Source: AMFI, Nuvama Research

The question is: will this trend sustain? And, what are the possible implications that might piggyback

this scenario? Naturally, we look to history for inspiration, and history rarely disappoints. We share the

learnings from the US of the 1980s and the 1990s.

India: Mirrors post-1970s’ US?

Similarities from the US of the 1970s can be found in the India of today: the most apparent being similar

per capita income levels and demography. This offers a good starting point. India and

1970s US have

Another hard-to-miss similarity is stagflation post-1970s. During this time, the Reagan administration similarities in

had unveiled significant reforms: capital markets were deregulated, tax rates were reduced and terms of per

capital allocation was left to private participants. In India too, post-stagflation in the early 2010s, capita GDP and

a large number of reforms were rolled out, and India’s capital markets now play a more active role Demography

in the economy.

115