Page 25 - Nuvama | IC Report 2023

P. 25

INDIA: THE 5D ADVANTAGE

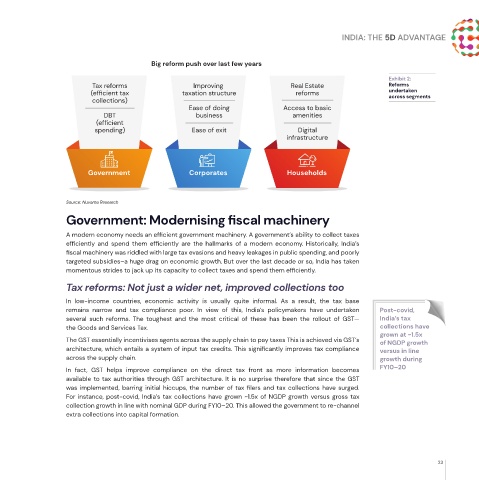

Big reform push over last few years

Exhibit 2:

Tax reforms Improving Real Estate Reforms

(efficient tax taxation structure reforms undertaken

across segments

collections)

Ease of doing Access to basic

DBT business amenities

(efficient

spending) Ease of exit Digital

infrastructure

Government Corporates Households

Source: Nuvama Research

Government: Modernising fiscal machinery

A modern economy needs an efficient government machinery. A government’s ability to collect taxes

efficiently and spend them efficiently are the hallmarks of a modern economy. Historically, India’s

fiscal machinery was riddled with large tax evasions and heavy leakages in public spending, and poorly

targeted subsidies–a huge drag on economic growth. But over the last decade or so, India has taken

momentous strides to jack up its capacity to collect taxes and spend them efficiently.

Tax reforms: Not just a wider net, improved collections too

In low-income countries, economic activity is usually quite informal. As a result, the tax base

remains narrow and tax compliance poor. In view of this, India’s policymakers have undertaken Post-covid,

several such reforms. The toughest and the most critical of these has been the rollout of GST— India’s tax

the Goods and Services Tax. collections have

grown at ~1.5x

The GST essentially incentivises agents across the supply chain to pay taxes This is achieved via GST’s of NGDP growth

architecture, which entails a system of input tax credits. This significantly improves tax compliance versus in line

across the supply chain. growth during

In fact, GST helps improve compliance on the direct tax front as more information becomes FY10–20

available to tax authorities through GST architecture. It is no surprise therefore that since the GST

was implemented, barring initial hiccups, the number of tax filers and tax collections have surged.

For instance, post-covid, India’s tax collections have grown ~1.5x of NGDP growth versus gross tax

collection growth in line with nominal GDP during FY10–20. This allowed the government to re-channel

extra collections into capital formation.

23