Page 19 - Nuvama | IC Report 2023

P. 19

INDIA: THE 5D ADVANTAGE

Relations with Russia (another large energy producer) while never cordial, have taken a turn for the

worse in the wake of the Ukraine war and freezing of Russia’s forex reserves by the US and others. What if this

Although early days, but Russia has begun to sell its energy in currencies other than the greenback. process of de-

What if this process of de-dollarisation of energy markets gains currency? dollarisation of

energy markets

As regards the second leg of the dollar system, the US-China relations have taken a turn for the worse. gains currency?

It set off with Trump’s tariff war, but anti-China sentiment spread during the pandemic. Of late, the US

is attempting to exclude Chinese firms such as Huawei from global markets and deny them access to

key inputs, ostensibly on national security grounds. This is fuelling China’s concerns that the US wants

to undermine its economy.

25

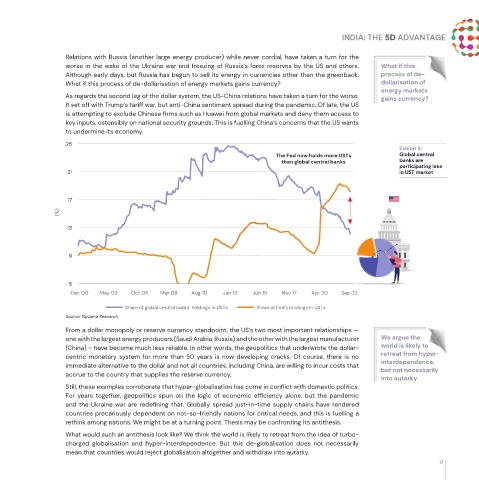

Exhibit 5:

The Fed now holds more USTs Global central

than global central banks banks are

participating less

21 in UST market

17

(%)

13

9

5

Dec 00 May 03 Oct 05 Mar 08 Aug 10 Jan 13 Jun 15 Nov 17 Apr 20 Sep 22

Share of global central banks’ holdings in USTs Share of Fed’s holdings in USTs

Source: Nuvama Research

From a dollar monopoly or reserve currency standpoint, the US’s two most important relationships —

one with the largest energy producers (Saudi Arabia, Russia) and the other with the largest manufacturer We argue the

(China) – have become much less reliable. In other words, the geopolitics that underwrote the dollar- world is likely to

centric monetary system for more than 50 years is now developing cracks. Of course, there is no retreat from hyper-

immediate alternative to the dollar and not all countries, including China, are willing to incur costs that interdependence,

but not necessarily

accrue to the country that supplies the reserve currency.

into autarky

Still, these examples corroborate that hyper-globalisation has come in conflict with domestic politics.

For years together, geopolitics spun on the logic of economic efficiency alone, but the pandemic

and the Ukraine war are redefining that. Globally spread just-in-time supply chains have rendered

countries precariously dependent on not-so-friendly nations for critical needs, and this is fuelling a

rethink among nations. We might be at a turning point. Thesis may be confronting its antithesis.

What would such an antithesis look like? We think the world is likely to retreat from the idea of turbo-

charged globalisation and hyper-interdependence. But this de-globalisation does not necessarily

mean that countries would reject globalisation altogether and withdraw into autarky.

17